2026 Winter Economic Forum

What better way to spend the evening before Valentine's Day than talking economics? On Friday, February 13, 2026, the UCSB Economic Forecast Project invited the new UC Santa Barbara Chancellor, Dennis Assanis; the new president and CEO of the Santa Barbara Zoo, Charles Hopper; and Dr. Peter Rupert to discuss the future and the challenges facing their organizations.

The new UC Santa Barbara Chancellor Dennis Assanis

opened with a proud moment for the university: on December 10, 2025, Professor Emeritus John Martinis and Professor Michel Devoret accepted Nobel Prizes in Physics in Sweden "for the discovery of macroscopic quantum mechanical tunnelling and energy quantisation in an electric circuit" — a landmark achievement that underscores UCSB's standing as a world-class research institution. That reputation is reflected in the rankings as well, with Forbes placing UCSB at No. 12 among public universities nationally and No. 42 overall.

Looking ahead, the Chancellor highlighted several exciting initiatives in the pipeline. On the academic side, UCSB is launching a new Bachelor of Science in Artificial Intelligence — designed to equip students with both the technical foundation and the ethical literacy to navigate an AI-driven world — alongside a new online Master's Program in Engineering and Technology Leadership offering tracks in Semiconductor Technology and Technology Management. To address the persistent challenge of student housing, two new residential projects will add over 3,400 beds to campus.

The Chancellor also touched on the university's growing momentum across several fronts: advances in quantum technologies and UCSB-born startups, the continued success of Arts & Lectures in drawing high-profile speakers and performers, and a remarkable stretch of athletic hosting duties — including the US Women's National Soccer Team, Team Austria's basecamp for the FIFA World Cup in June 2026, and delegations preparing for the LA 2028 Olympics and Paralympics.

Perhaps the most locally significant announcement was that UCSB is coming to State Street. The university's acquisition of a mixed-use portfolio on State and Gutierrez streets — encompassing substantial commercial space and a residential building — plants the university in the heart of downtown Santa Barbara and positions it as a potential anchor for the revitalization of the business district.

The new President and CEO of the Santa Barbara Zoo, Charles Hopper

made a compelling case about how the Zoo is one of Santa Barbara's most important economic and civic institutions. The Zoo welcomed 478,634 guests in 2024, making it the #1 museum and attraction by attendance in the Tri-Counties region. Zooming out to the national level, a 2024 economic impact study of AZA-accredited zoos and aquariums found that institutions like the Santa Barbara Zoo collectively generate $35 billion in economic impact, support more than 254,000 full-time jobs, and serve over 209 million visitors annually.

Perhaps the most exciting development shared at the Forum was the planned Santa Barbara Zoo Conservation Center at California State University Channel Islands. The facility will include a Wildlife Recovery Center, Veterinary Center, Animal Nutrition Center, and Conservation Hub — a genuine research and conservation infrastructure that ties the Zoo's mission directly to higher education and workforce development in the region. This partnership with CSUCI represents the kind of institutional collaboration that can produce lasting economic and environmental dividends.

The Zoo's conservation work spans the broader Central Coast ecosystem, with active programs supporting species including the California Condor, Island Fox, Southern Sea Otter, Western Snowy Plover, and California Tiger Salamander, among others.

The Zoo's 2026–2030 Strategic Plan makes its ambitions explicit. Under the four pillars of People, Place, Purpose, and Performance, the Zoo has set a goal of becoming the best employer in Santa Barbara — a meaningful commitment in a labor market where housing and cost-of-living challenges make talent retention difficult for everyone.

Last up was EFP's own Peter Rupert

who gave an Economic Update of the county and nation, and shared a video teasing new data and initiatives, made by one of EFP's new social media interns. Peter then challenged the audience to question what they think they know about the U.S. economy by showing a TEDTalk that emphasizes that people have a high statistical chance of being quite wrong about what they think they know.

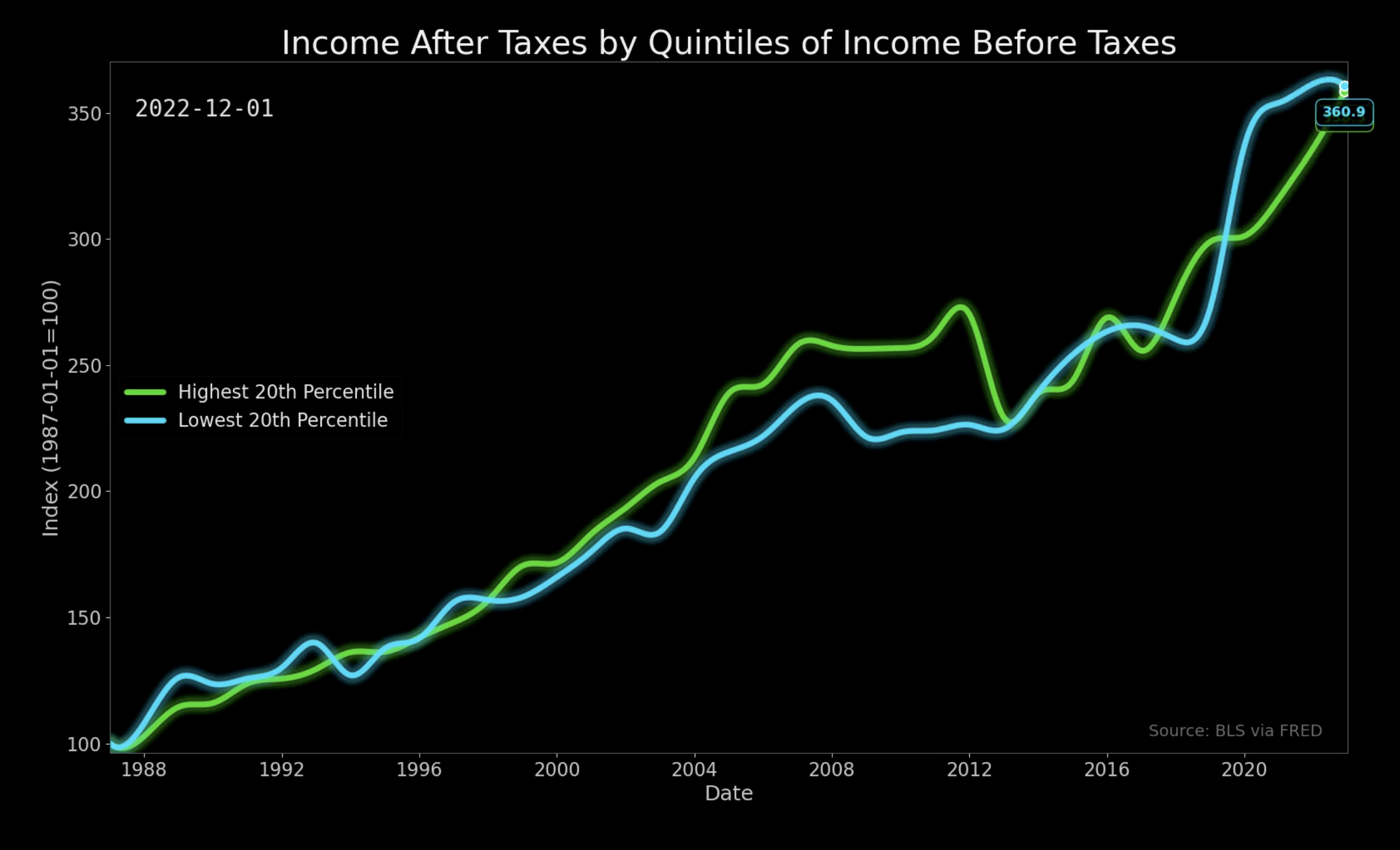

Posing the question, "how does income growth of the bottom 20% compare to the top 20%?" The graph below tracks after-tax income growth for the top and bottom 20% of earners from 1987 to 2022, indexed so that both groups start at 100 in 1987. By 2022, the lowest quintile (360.9) had actually outpaced the highest quintile in indexed growth. This is counterintuitive given most inequality narratives, but there are important nuances to consider.

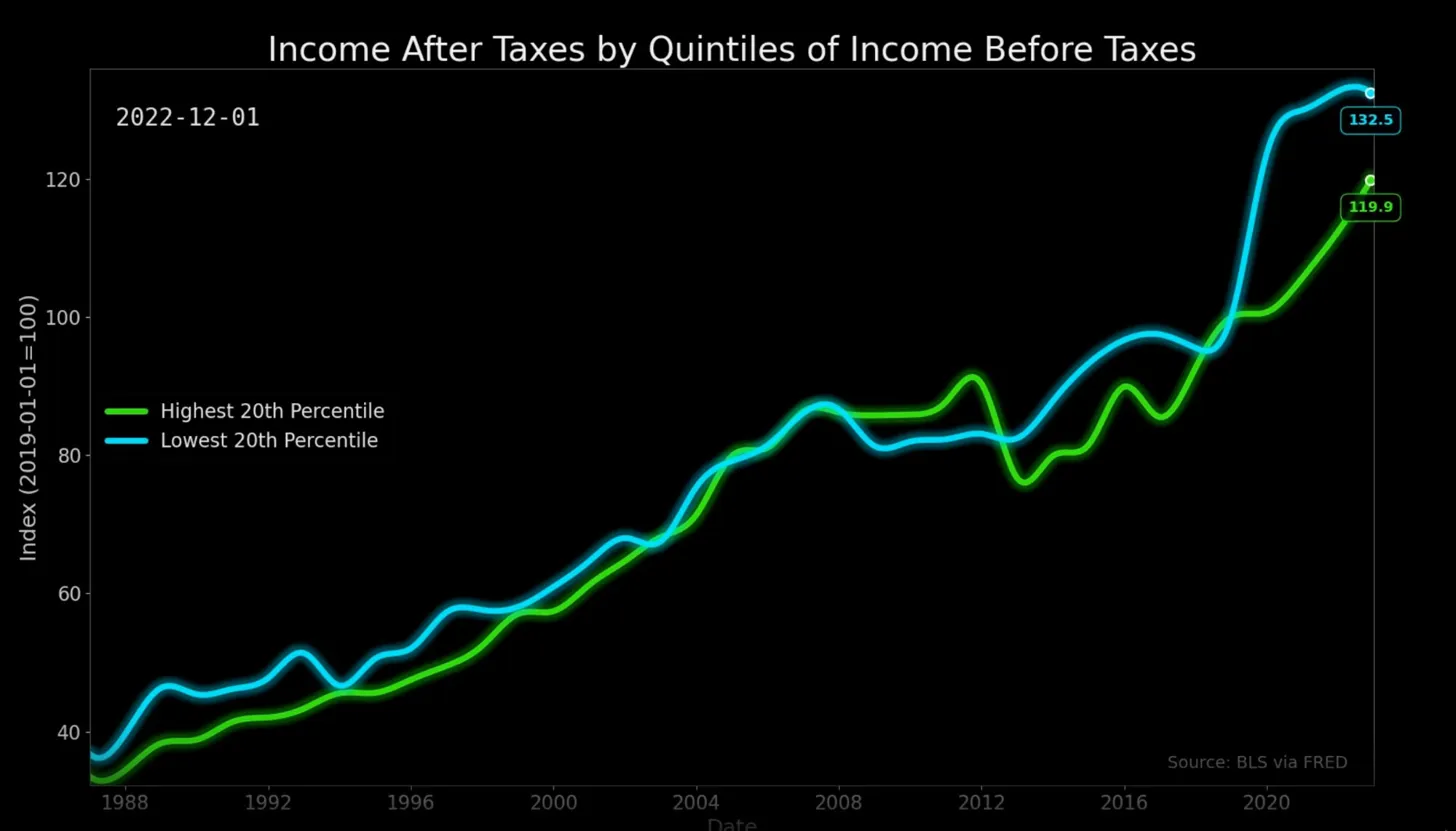

Now... using the same data, but re-indexing to 2019 = 100 instead of 1987 = 100. That single change tells a very different story. What stands out immediately is that the lowest quintile (132.5) has dramatically outpaced the highest quintile (119.9) when you zoom in on the recent period. The gap is much more visually pronounced here than in the first chart.

Peter than talked about the U.S. economy's remarkable resilience and long-run strength. After a brief contraction in Q1 2025 (-0.6%), real GDP growth rebounded sharply to 3.8% and 4.4% in the following two quarters, continuing a pattern of solid post-pandemic expansion. On a per capita basis, real GDP has grown nearly tenfold since 1950 — from roughly $7,000 to nearly $70,000 in 2017 dollars — with recessions appearing as only minor interruptions to an otherwise steady upward trajectory. Perhaps most striking from the data Peter presented is the international comparison: since 1995, U.S. real GDP per capita has grown to 160 (index) versus just 141 for the Euro20 area, a gap that was modest through the early 2000s but widened decisively.

The U.S. labor market picture is more nuanced than the headline weakness narrative suggests. Total U.S. payroll employment has been choppy — with notable negative months in January 2025, June, August, and a sharp -140,000 in October 2025 — but the January 2026 reading of +130,000 and consistently positive private payroll growth (including +172,000 in January 2026) suggest the private sector has remained the steadier engine of job creation throughout. The unemployment and job openings data tells a broader story of normalization: after the historic post-pandemic mismatch when job openings briefly exceeded unemployed persons, both series have converged back toward roughly 7–8 million, a level consistent with a healthy but no longer overheated labor market — tight by pre-2020 historical standards, but no longer the frenzied hiring environment of 2021–2022.

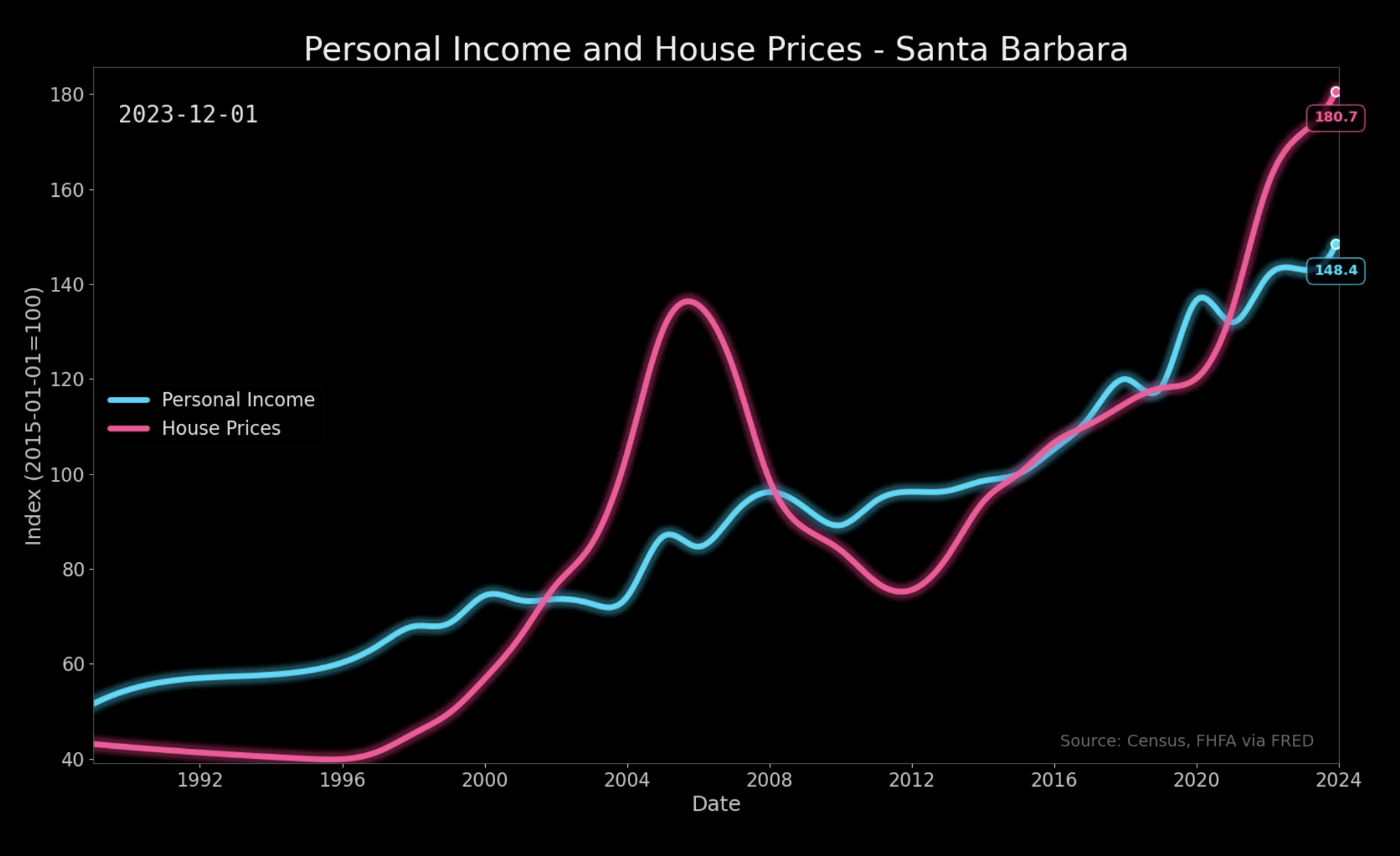

Below you can see that house prices spiked sharply during the 2000s bubble, crashed, then recovered — but the post-2020 surge has been particularly steep, with prices now at 180.7 against a personal income index of just 148.4 (both indexed to 2015). The widening gap between the two lines in recent years reflects how quickly homeownership has moved out of reach for typical Santa Barbara residents.

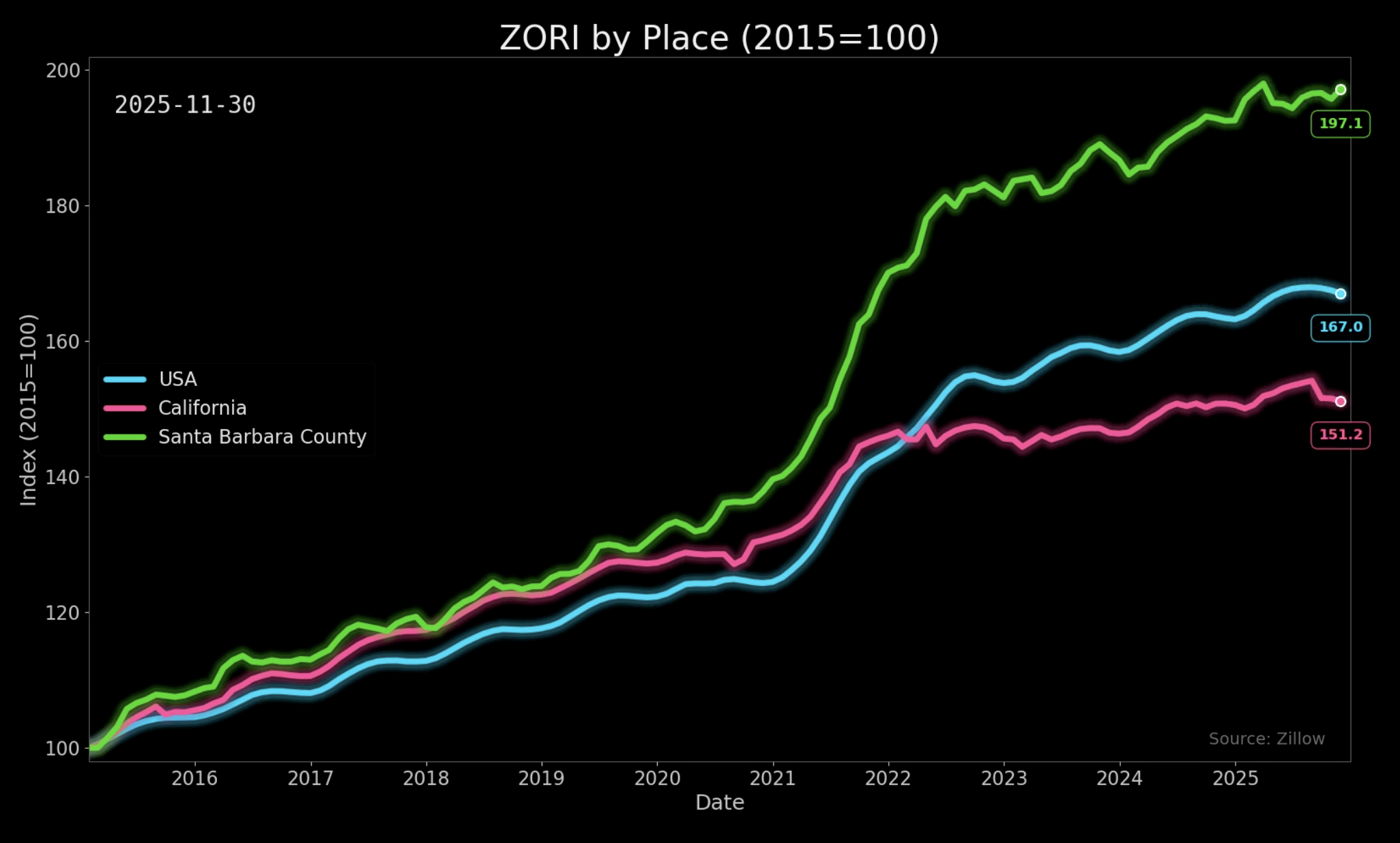

Now turning to Zillow Observed Rent Index (ZORI), Santa Barbara County rents have nearly doubled since 2015, reaching an index of 197 — well above the national average of 167 and California's 151. The county's rent growth accelerated dramatically between 2020 and 2022 before leveling off slightly, but it has continued climbing while California rents have largely plateaued. This means renters in Santa Barbara have faced disproportionately intense cost pressure compared to both state and national peers.

Why is this happening? Basic economics offers a clear answer: when regulations increase the cost of building or rent control policies reduce the financial incentive to supply housing, the result is less housing — and less housing means higher prices. Santa Barbara is a particularly acute case, where geographic constraints, restrictive zoning, and limited new construction have compounded these pressures for decades, leaving both renters and prospective buyers increasingly priced out of the market.

The evening closed with a lively Q&A that gave the audience a chance to engage directly with the Chancellor, Charles, and Peter — sparking candid conversation and no shortage of thoughtful perspectives on the challenges and opportunities ahead for Santa Barbara.

Events like this don't come around often — an evening of genuine conversation with some of Santa Barbara's most influential voices on the economy, higher education, and the future of our community. If you'd like to be in the room for the next one, we'd love to have you. Reach out to elj@ucsb.edu to learn more about sponsorship opportunities, which includes access to our sponsor-exclusive Winter 2027 forum and a range of other benefits that keep you connected to the pulse of the Santa Barbara economy year-round.

Access Charles Hopper's slides here.